What Is Equipment Breakdown Coverage on a Homeowners Insurance Policy?

- Bergen Insurance Group

- May 1

- 4 min read

Bergen Insurance Group | Home Insurance Education

Many homeowners assume their homeowners insurance policy covers every type of appliance or equipment failure inside the home.

However, standard homeowners insurance policies are generally designed to cover:

sudden accidental direct physical loss

from covered causes such as:

fire

wind

theft

lightning

certain water damage

Mechanical failure, electrical burnout, and internal equipment malfunction are often handled differently.

This is where: Equipment Breakdown Coverage

may become valuable.

At Bergen Insurance Group, we help New Jersey homeowners better understand how Equipment Breakdown Coverage works, what it may cover, and how it differs from a traditional home warranty plan.

What Is Equipment Breakdown Coverage?

Equipment Breakdown Coverage is generally an optional endorsement added to a homeowners insurance policy that may help cover certain sudden mechanical or electrical failures involving home systems and appliances.

Depending on the policy structure, covered equipment may sometimes include:

HVAC systems

central air conditioning

furnaces

water heaters

refrigerators

washers and dryers

electrical panels

built-in appliances

smart home systems

electronics

Coverage availability and policy wording vary by insurance company.

How Equipment Breakdown Coverage Differs From Standard Homeowners Insurance

Standard homeowners insurance policies typically focus on: external causes of loss

such as:

fire

lightning

windstorm

vandalism

theft

Equipment Breakdown Coverage is different because it may help cover: internal mechanical or electrical failure involving certain systems or appliances.

This distinction is important because many homeowners are surprised to learn that appliance breakdown alone may not automatically fall under standard homeowners insurance coverage.

Real-World Claim Examples

Example 1: HVAC Compressor Burnout

A central air conditioning compressor suddenly experiences electrical burnout during a summer heatwave.

Depending on the policy wording, Equipment Breakdown Coverage may potentially help cover:

repair costs

replacement costs

labor expenses

for the failed system.

Example 2: Electrical Surge Damages Appliances

A sudden power surge damages:

refrigerator

microwave

washer and dryer

smart home devices

Depending on the endorsement structure, Equipment Breakdown Coverage may potentially help with certain

damaged equipment caused by electrical failure or power surge events.

Example 3: Water Heater Mechanical Failure

A water heater suddenly stops functioning due to internal mechanical failure.

While normal aging or gradual wear may generally be excluded, certain sudden covered breakdown events may potentially qualify depending on the policy wording.

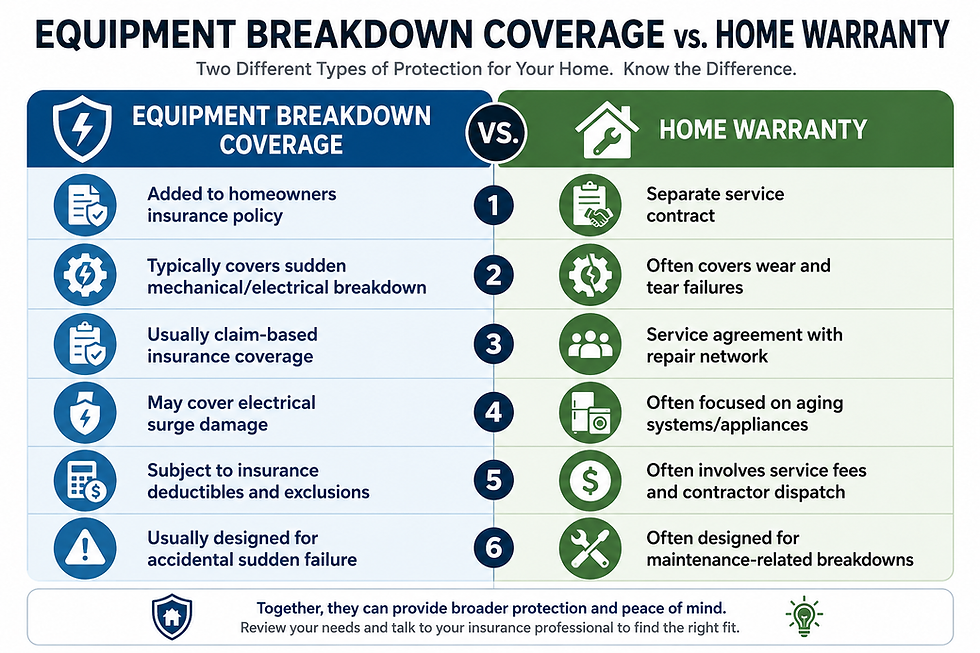

Equipment Breakdown Coverage vs Home Warranty

Many homeowners confuse: Equipment Breakdown Coverage and Home Warranties because both may involve appliance or system repairs.

However, they function very differently.

Key Differences Between Equipment Breakdown Coverage and Home Warranties

What Equipment Breakdown Coverage Typically Does NOT Cover

Equipment Breakdown Coverage commonly does not apply to:

normal wear and tear

gradual deterioration

rust or corrosion

lack of maintenance

cosmetic damage

pre-existing issues

Coverage generally focuses on: sudden accidental mechanical or electrical breakdown.

This is one reason homeowners should continue properly maintaining:

HVAC systems

appliances

plumbing

electrical systems

even when Equipment Breakdown Coverage is added.

Why This Coverage Is Becoming More Important

Modern homes now rely heavily on:

smart appliances

integrated HVAC systems

electronics

computerized equipment

advanced electrical systems

As homes become more technology-dependent, the cost to repair or replace failed systems may increase significantly.

This is one reason many homeowners review Equipment Breakdown Coverage as part of a broader homeowners insurance review.

Important Coverage Considerations

Equipment Breakdown Coverage may involve:

coverage limits

deductible structure

exclusions

repair vs replacement provisions

age restrictions

maintenance requirements

Because policy structures vary, homeowners should carefully review:

covered equipment

exclusions

endorsement limits

deductibles

policy wording

with their insurance advisor.

Why Independent Insurance Advice Matters

Different insurance companies may:

structure Equipment Breakdown Coverage differently

define covered equipment differently

apply different exclusions

limit older systems

offer different endorsement limits

Independent insurance agencies can help homeowners:

review equipment exposure

compare coverage options

understand potential gaps

evaluate protection for major home systems

At Bergen Insurance Group, we help New Jersey homeowners better understand optional homeowners insurance coverages before costly equipment failures and unexpected losses occur.

FAQs

What is Equipment Breakdown Coverage?

Equipment Breakdown Coverage is generally an optional homeowners insurance endorsement that may help cover certain sudden mechanical or electrical failures involving home systems and appliances.

Is Equipment Breakdown Coverage the same as a home warranty?

No. Equipment Breakdown Coverage is generally an insurance endorsement focused on sudden accidental breakdown, while a home warranty is usually a service contract designed for appliance and system repair needs.

Does homeowners insurance cover appliance breakdown?

Not always. Standard homeowners insurance policies generally do not cover normal appliance breakdown or internal mechanical failure unless caused by a covered peril.

Does Equipment Breakdown Coverage cover wear and tear?

Typically no. Normal aging, deterioration, corrosion, and maintenance-related issues are commonly excluded.

Other Suggested Articles

Disclaimer

The information provided in this article is intended for general informational purposes only and should not be interpreted as insurance, legal, mechanical, electrical, warranty, or financial advice. Coverage availability, exclusions, deductibles, endorsement structures, and policy wording vary by insurance company and individual situation. Please contact Bergen Insurance Group to review your specific homeowners insurance and Equipment Breakdown Coverage options.

Comments