Why Insurance Companies Ask When Your Electrical Was Updated

- Vincent Fuccilli

- 2 days ago

- 5 min read

Bergen Insurance Group | Home Insurance Education

When applying for homeowners insurance in New Jersey, many homeowners are surprised by a question that seems difficult to answer—especially buyers of older homes built before modern electrical standards existed.

"What year was the electrical system updated?"

Unlike a roof or furnace, electrical systems are often updated gradually over many years. A panel may have been replaced, some circuits may have been rewired, and outlets may have been upgraded at different times.

So why do insurance companies care?

The answer is simple: older electrical systems are one of the leading causes of residential fires and insurance claims.

As insurance companies continue to tighten underwriting standards, the age and condition of a home's electrical system has become one of the most important factors in determining eligibility and pricing.

Why Electrical Systems Matter to Insurance Companies

Insurance companies are not necessarily concerned with the age of your home.

Instead, they are concerned with the condition and safety of the systems inside the home.

An older home that has been properly maintained and updated may be easier to insure than a newer home with outdated electrical components.

Electrical issues can increase the risk of:

Electrical fires

Power surges

Arc faults

Property damage

Liability exposures

For this reason, many insurance companies now ask detailed questions about electrical systems during the application process.

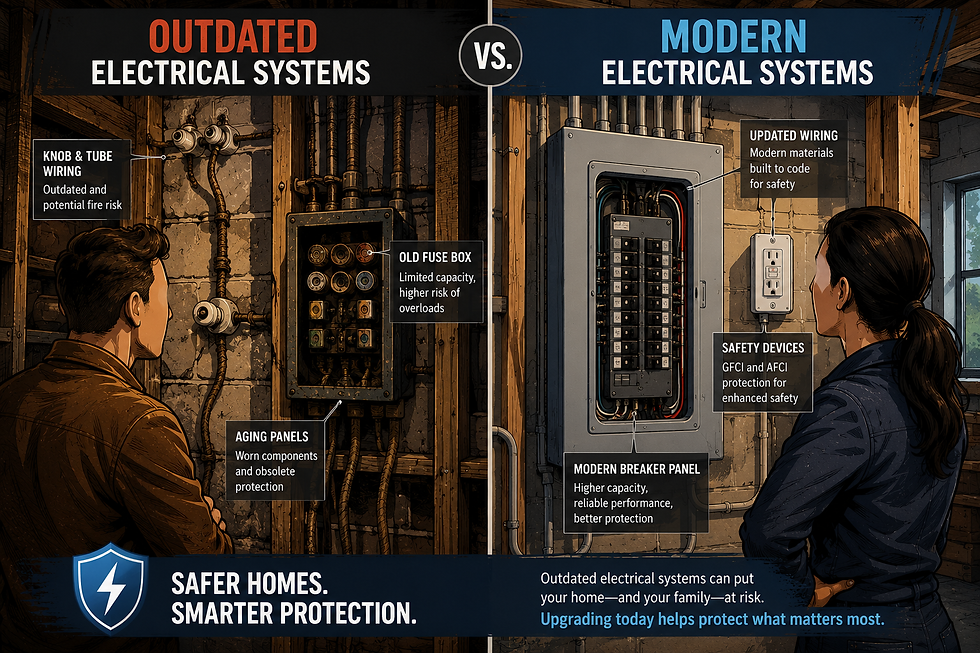

What Counts as an Electrical Update?

One of the biggest misconceptions among homeowners is that replacing a few outlets means the electrical system has been updated.

Insurance companies typically look for major improvements such as:

Electrical Panel Replacement

Replacing an outdated electrical panel with a modern breaker panel is one of the most significant upgrades.

Examples include replacing:

Federal Pacific panels

Fuse boxes

Zinsco panels

Obsolete breaker panels

Service Upgrade

Increasing electrical service from:

60 amp

100 amp

to:

150 amp

200 amp

can significantly improve insurability.

Rewiring

Replacing outdated branch wiring with modern wiring materials.

Examples include:

Knob-and-tube replacement

Aluminum wiring remediation

Partial or complete rewiring

Safety Device Upgrades

Installation of:

GFCI protection

AFCI protection

Updated grounding systems

can improve electrical safety.

What If Only Part of the Electrical System Was Updated?

his is one of the most common questions homeowners ask.

Many older homes have been updated gradually over time rather than through a complete electrical renovation.

For example:

The electrical panel may have been replaced in 2015.

The kitchen may have been rewired during a remodel.

Bathroom outlets may have been upgraded with GFCI protection.

Portions of the original wiring may still remain elsewhere in the home.

In these situations, the answer is often not as simple as providing a single update year.

Insurance companies may want to know:

When the panel was replaced

Whether any original wiring remains

Whether knob-and-tube wiring is still active

Whether aluminum wiring is present

Whether the electrical service was upgraded

This is why two homes with the same construction year may be viewed very differently by insurance companies.

A home with a new 200-amp service, updated breaker panel, and rewired living areas may qualify for more insurance options than a similar home that still contains significant portions of its original electrical system.

If you're unsure how to answer these questions, an electrician's report, municipal permit records, or documentation from prior renovations may help determine what updates have been completed.

Common Electrical Issues That Create Insurance Problems

Certain electrical conditions frequently create underwriting concerns.

Knob-and-Tube Wiring

Knob-and-tube wiring was commonly installed in homes built before the 1940s.

While some systems may still function properly, many insurance companies will not insure homes with active knob-and-tube wiring.

Aluminum Wiring

Aluminum branch wiring was commonly installed during the 1960s and 1970s.

Over time, loose connections can develop and create fire hazards.

Some insurance companies require documentation showing approved remediation methods.

Federal Pacific Panels

Federal Pacific Electric (FPE) panels have become one of the most discussed electrical concerns in homeowners insurance.

Many insurance carriers consider these panels unacceptable due to documented safety concerns and may require replacement before coverage can be written.

Fuse Boxes

Some older fuse systems remain in service today.

Depending on the carrier and condition of the system, fuse boxes may limit available insurance options.

Why Homeowners Often Don't Know the Answer

Many homeowners genuinely do not know when their electrical system was updated.

This is especially common when:

The home was purchased recently

Renovations were completed by previous owners

Records were never transferred

Updates were performed gradually over time

This is one reason insurance carriers may request additional information, photographs, inspection reports, or clarification before issuing a policy.

Buying an Older Home? Check These Items Before Closing

If you are purchasing an older home in New Jersey, consider reviewing:

✓ Electrical panel manufacturer

✓ Electrical service size

✓ Presence of knob-and-tube wiring

✓ Presence of aluminum wiring

✓ Date of major electrical upgrades

✓ Home inspection findings

Addressing these issues before closing can help prevent delays during the insurance process.

Real-World Example

Imagine two homes built in 1925.

Home A

Original fuse box

Active knob-and-tube wiring

No major electrical updates

Home B

Modern 200-amp service

Updated breaker panel

Rewired circuits

GFCI and AFCI protection

Although both homes were built in the same year, Home B will generally have significantly more insurance options available.

The age of the home is often less important than the condition of its major systems.

The Bottom Line

When an insurance company asks when your electrical system was updated, they are trying to understand the overall safety and condition of the home.

Older homes can absolutely be insured, but insurance companies increasingly focus on updated electrical systems, roofing, plumbing, and heating equipment when evaluating eligibility.

If you are unsure about the age or condition of your electrical system, working with a knowledgeable independent insurance agency can help identify potential issues before they become obstacles to obtaining coverage.

Frequently Asked Questions

Why does homeowners insurance ask when my electrical was updated?

Insurance companies use this information to evaluate fire risk and determine whether a home's electrical system meets their underwriting guidelines.

Can I get homeowners insurance with knob-and-tube wiring?

Most likely not in NJ through a standard carrier. Some insurance companies may offer coverage, while others may require replacement or additional review. Availability varies by carrier.

Is aluminum wiring a problem for homeowners insurance?

It can be. Some insurance companies require documentation showing approved remediation methods have been completed.

What is a Federal Pacific electrical panel?

Federal Pacific Electric (FPE) panels are older electrical panels that many insurance companies view as higher risk due to safety concerns.

Does replacing my electrical panel lower my insurance premium?

Not necessarily. However, replacing an outdated panel may improve eligibility with more insurance companies and reduce underwriting concerns.

How can I find out when my electrical system was updated?

A licensed electrician, municipal permit records, home inspection reports, or prior owner documentation may help determine when major electrical work was completed.

Other Suggested Articles

Disclaimer: This article is for general educational purposes only and does not guarantee coverage, eligibility, pricing, or claim outcomes. Insurance underwriting guidelines vary by company, policy form, property condition, location, and individual circumstances. Always review your specific policy and speak with a licensed insurance professional before making coverage decisions.

Comments